I’d like to offer some condolences in this introduction, but I’m not sure how much better a blog post from a stranger can make you feel at this time. So I’m going to get straight into it, instead. When a family member has died, here are the things you should do to keep your finances protected.

Table of Contents

Dealing with funeral costs

Perhaps the first financial worries many people have during this time will be in relation to the funeral. And most are not wrong to be worried. On average, a funeral can cost upwards of $6000. Sadly, many of those high costs are the result of funeral directors taking advantage of people when they are bereaved. You should do your best to be one your guard when “shopping” around for funeral services. There are several ways in which you can save money at any given funeral home. Some institutes may offer financial assistance for funerals, so be sure to research this.

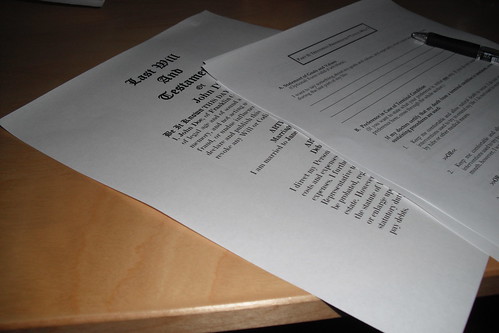

Getting help with the estate

There is a lot less complication in this area when someone has left behind a will. But recent polls suggest that a majority of people over the age of 35 don’t actually have a will set out at all. Whether or not a will is set out, getting assistance may be to your benefit. You could give responsibility for arrangements to a family member or a trusted friend, as this will save money. But if there are any legal complexities, then you may need more official legal help. Getting the right lawyer during the probate process can protect your finances and inheritance to a large degree.

Taxes

In America, a surviving family member may have a lot of responsibilities forced upon them by the IRS. Never ones to let death get in the way of profit, they may request a large amount of tax to be paid from the estate before you can legally inherit anything. Thankfully, this rarely means that you’ll be paying anything from a source outside of the assets in the estate. But make sure you research all the IRS information you can get. Knowing what to expect may help you protect yourself if they try to take more than the tax code actually permits them to take.

Their pension

You’re best taking this up with the company the deceased worked for most recently. Pensions in America aren’t bound up in many ‘universal’ laws. This means that some pensions may be payable to a surviving spouse or to any children. Many pension arrangements, however, end completely when someone dies. The money they had in that account will go back to the company (although some, of course, will go to the pockets of the IRS). Dig up any paperwork regarding the pension agreement. It may be best to seek legal advice in this area if you run into any trouble.

Bereavement and work

One worry that many will have is what to do about work. After all, bereavement may reduce your ability to work more than any illness! Thankfully, the state does have your back. You are entitled to paid leave for bereavement in most states. Other states may use credit hours arrangements or alternative work schedules. But whatever the state laws say, it’s something you should discuss with your employer. I doubt there are many employers who will deny you some paid time off in these circumstances.

Image credit:

Image 1 – By Sam Caplat (https://www.flickr.com/photos/samcaplat/4521089467) [CC BY 2.0 (http://creativecommons.org/licenses/by/2.0)], via Wikimedia Commons

Image 2 – Ken Mayer – https://flic.kr/p/9wP4Sf

Image 3 – Philip Ingham – https://flic.kr/p/wysZd